A New UAS Paradigm

Feb 8th, 2016

by Prateep Basu, NSR

Unmanned Aerial Systems (UAS) have been utilized for more than

three decades, but their diversity increased only recently, with

explosive growth in small UAS (sUAS) sector. The impact of these

sUAS on satellite services such as Communications and Earth

Observation is difficult to assess, and more so with increasing

technological sophistication in both satellites and UAS.

UAS Industry

Value Pyramid by Airframe Type

In NSR’s UAS Satcom & Imaging Markets,

2nd Edition, UAS markets were analyzed and two segments

were assessed: UAS for Satcom and UAS for Imaging. With mainstream

media focusing on these UAS and other High Altitude Platforms (HAPs)

due to the involvement of tech-giants like Google and Facebook (who

want to provide Internet to the unconnected), along with a

booming sUAS market that has seen acquisitions and investments by

established companies like Intel and Amazon,

NSR believes the UAS industry will be an

externality for satellite industry growth.

UAS Helps Satcom Markets

HALE and MALE UAS like the Global Hawk

and Reapers use Satcom Common Data Links (CDL) for Beyond

Line-Of-Sight (BLOS) communications, and have been a steady source

of revenues for GEO communication satellite operators. However, with

payloads such as SAR, EO/IR

cameras, and applications like full-motion video, bandwidth needs of

UAS have risen tremendously, though the airframe designs haven’t

evolved to take advantage of HTS services yet.

The usage of inclined satellite capacity, especially over regions

where demand is high (like Africa and the Middle-East) has

alleviated costs for the U.S. DoD, which operates the largest fleet

of such UAS. But, NSR

expects a transition to GEO-HTS for these UAS from the mostly FSS

Ku-band equipment,

and in particular to GEO-HTS Ku-band due to the easier retrofits

required. Apart from lower

cost/bit and more bandwidth, GEO-HTS is naturally resilient to

signal jamming as there are multiple beams that need to be jammed,

and that too from within an HTS beam’s coverage area, which is only

a few hundred kilometers wide, making it an attractive proposition

for carrying UAS. Additionally, the advancements in low profile,

bandwidth efficient, and lightweight electronically steered

antennas, combined with the next-generation of satellite modems,

will bring about paradigm shifts in the way UAS are operated.

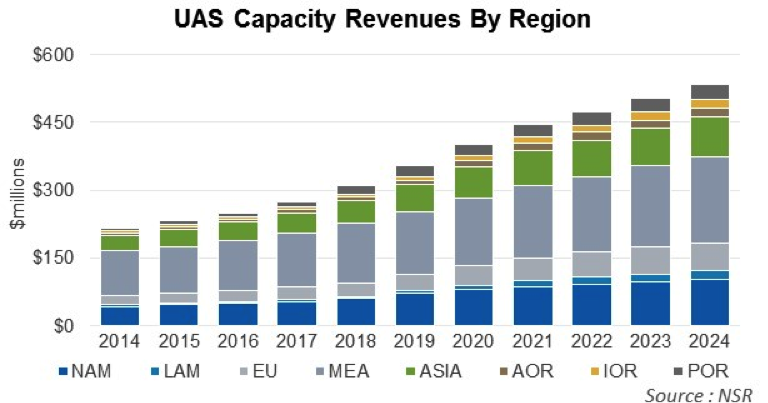

NSR expects satellite

capacity to UAS revenues to grow to $534 million by 2024, at a CAGR

of 9.4%, largely driven by such changes in UAS operations on Satcom.

UAS Imaging Competes with

Satellite

NSR analyzed the sUAS sector imaging

applications market and noted

opportunity in this industry lies in the

software and services,

which even the industry leader DJI understands by launching its

operating system. The biggest

contribution of this upcoming sUAS industry has been the integration

of technologies, and the rate at

which its refresh puts Moore’s law in the backseat. Recently,

Precision Hawk, Verizon, Digital Globe, and Harris announced

completion of phase 1 testing of an UAS airspace management system,

utilizing Digital Globe’s high-resolution Earth images, Verizon’s

LTE network, and Harris’ satellite-based surveillance (ADS-B) for

safe UAS operations in civilian airspace.

Such seamless integration and

commercialization of satellite and terrestrial technology opens the

gates for a multitude of applications,

specifically those related to Internet of

Things (IoT), by using the UAV as a sensor.

In the same UAS report, NSR found that photogrammetry

applications (like creating a 3D point cloud or ortho-mosaics) have

advanced rapidly, and the turnaround time for image processing has

decreased, which reduces

the competitive advantages of satellite-based Earth imaging.

However, cost of sUAS imaging can be prohibitive for large corridor

mapping, and NSR sees a mixed

approach being gradually taken by both sUAS and satellite-EO

industry, with image fusion

creating layered maps for vertical markets such as agriculture,

energy, and resource management.

Thus, sUAS imaging can be expected to push the satellite

industry’s penetration in new markets, but also act as a pull for

its growth due to the competing nature of the technology.

Bottom Line

UAS have revolutionized the way wars

are fought, and now sUAS are commoditizing imaging and consumer data

analytics. Some have touted this decade as “the one” for UAS, given

explosive growth in all types of airframes, avionics, and associated

software. As the fastest growing sector in aerospace,

NSR expects

the UAS segment to act both as a

‘push’ and a ‘pull’ for the satellite industry over the period of

time, with Satcom for UAS

generating the bulk of the revenues and sUAS imaging leading the

innovation on the technological front.