NSR Financial Roundup of 2014 & H1 2015

Oct 20th, 2015 by Blaine Curcio, NSR

The past 18 months have brought forth some of the most

sweeping changes the satellite telecom industry has ever seen.

Known for years as an insulated industry that grew at GDP-like

growth rates, we have recently seen completely new words and

concepts enter our lexicon and consciousness—unicorns, LEO-HTS

constellations, rounds of funding in the hundreds of millions of

dollars despite no proven revenue generation whatsoever. This

has led to whispers of pricing pressures, increased competition,

and new applications being unlocked as orders of magnitude more

capacity are put into orbit.

In its latest report, Satellite Operator Financial Analysis,

5th Edition (SOFA5), NSR assessed operator financial health by

examining issues at a macro level, analyzed industry-wide

metrics, while also digging into individual operator metrics.

Three key highlights and trends of the past 18 months are

noteworthy:

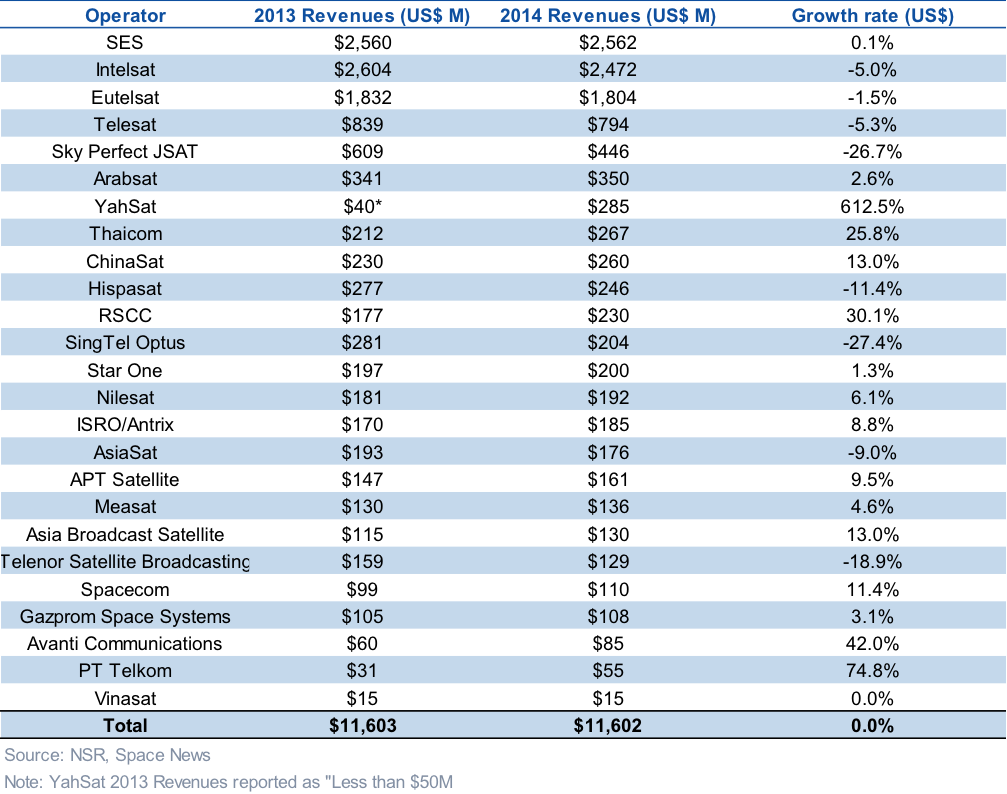

SES Overtakes Intelsat in Top-Line Revenues….Temporarily

Full-year 2014 financials saw some degree of shake-up among

operators, with currency exchange rates and varying degrees of

exposure to contracting markets such as Gov/Mil causing some

movement among top operators. Notable, SES overtook Intelsat in

terms of top-line revenues in 2014, with the former’s revenues

of $2.562 billion besting the latter’s $2.472 billion. The two

operators traded places again in H1 2015, with Euro depreciation

negatively impacting SES’s dollar-denominated revenues, which

fell to just under $1.1 billion, well behind Intelsat’s $1.2

billion. The two operators have in recent years been on

different trajectories, with Intelsat hurting from exposure to

US Government clients, and SES weathering this storm more

effectively due to a somewhat less US-centric customer base.

Other operators reporting swings in revenues included Sky

Perfect JSAT, which saw a 15% drop in Yen-denominated revenues

correspond to a 26.7% drop in dollar-denominated revenues, due

to a weakening Yen, which has more likely than not bottomed out

vis-à-vis the USD. YahSat, Thaicom, and Avanti—all of whom rely

on GEO-HTS payloads for a significant percentage of revenues—saw

healthy revenue growth across the board. This lends further

credence to the idea that GEO-HTS will propel future industry

growth. Overall, the industry saw flat revenues in 2014, with

total revenues from the top 25 FSS operators remaining around

$11.6 billion.

Annual Revenues per Transponder Declined….Significantly

Annual revenues per leased FSS transponder among the 22

operators tracked in this metric declined from $2.05M to $1.94M

during the past year, with pricing pressures coming to fruition

through a combination of aforementioned currency exchange rate

fluctuations (for example, JSAT’s metric fell from $4.8M to

$3.4M, partially due to Yen depreciation) and lower pricing in

general. That said, the question of “will GEO-HTS grow the pie

as much as it shrinks the cost per slice?” has thus far yielded

an answer of yes, with the industry again having seen more or

less flat revenue growth in a year that saw shorter-term

macroeconomic headwinds, such as reduced government spending.

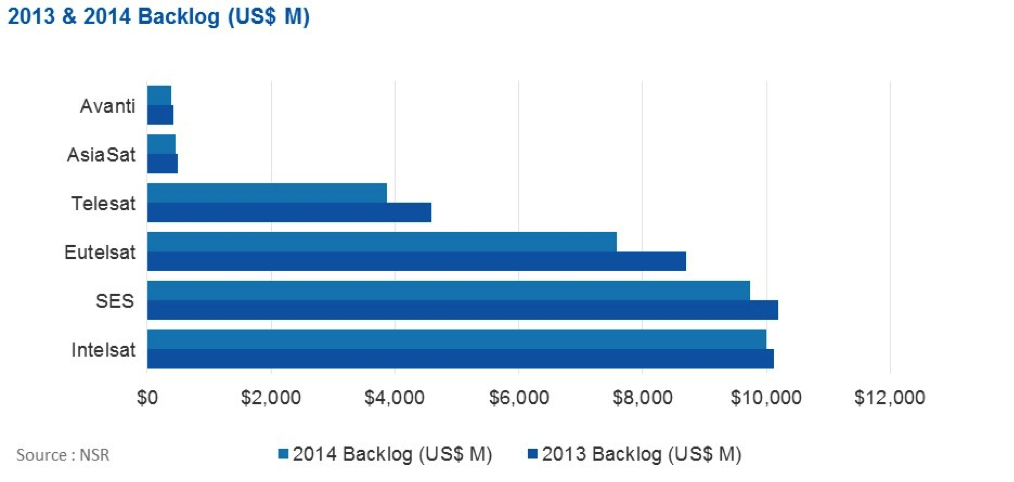

Operator Backlogs Declined….Universally

Only 6 operators report backlog figures, but in 2014, all 6

of them saw backlog decline. These six operators—the Big Four,

AsiaSat, and Avanti—saw collective backlog decline from $34.5

billion to $32.0 billion, indicating a wider transformation of

business models in the industry. Specifically, as a smaller

percentage of operator revenues comes from video, and a larger

percentage comes from data, average contract lengths will

decline, thus leading to less backlog overall. Some operators

will undoubtedly find this being a major issue, with increased

revenue volatility making it more difficult to raise capital and

much more difficult to pull the trigger on CAPEX decisions in

the hundreds of millions of dollars. Put another way, it’s a lot

more difficult to justify launching a $250M satellite when there

is no anchor client, and as the era of GEO-HTS systems continues

to dawn, the time of 15-year DTH anchor clients is running out.

Bottom Line

Lower government spending, increased volatility and mounting

price pressure, among others, form the competitive landscape

satellite operators are navigating in today and will continue to

traverse over the short-to-medium term. In a business that

requires a 15-year horizon or a 15-year bet, short-to-medium

term challenges will dictate the strategic direction of

individual players in adjusting to the shifting course of the

marketplace.

And here is what NSR sees…

The increased proliferation of GEO-HTS payloads has laid the

groundwork for some fundamental changes to the satellite

telecommunications industry and the business models therein.

Some operators have been able to capitalize on first-mover

advantages, while others will undeniably take a “wait and see”

approach that will put them at a disadvantage should the market

continue to evolve in ways that favor GEO-HTS business models

over the traditional paradigm, including more growth coming from

data applications rather than video. The latter camp of

operators is becoming increasingly isolated, with the latest

operator to switch sides on the GEO-HTS debate being APT

Satellite, which recently reversed years of “wait and see” with

a more proactive approach to GEO-HTS.

Overall, it is expected that moving forward, operators will

need to make up for a fall in prices by leasing significantly

more capacity, which will become feasible through a continued

preference for GEO-HTS systems. Traditional FSS will remain

relevant for point-to-multipoint communications (i.e. DTH), but

overall there remains limited reason for a new data-type

customer to choose FSS over GEO-HTS in many, but not all,

instances. In our next finance-oriented Bottom Line, NSR will

examine the impact of LEO-HTS constellations in the industry,

with emphasis on the impact of potential cannibalization and

continued pricing pressures due to excess capacity. And here,

business models will play a key role when all signs lead to

commoditization of capacity as satellite operators will be faced

with an onslaught of cheap bits flooding the marketplace, all

looking for that elusive “killer app.”